Although Vietnam’s senior housing market is supported by several positive factors, including rapid population aging, changes in traditional family structures, and the growth of the middle class, this segment has not yet developed into a clear and independent real estate market with strong liquidity and investment potential.

1. Rapid aging pressure and growing demand for specialized housing

According to the General Statistics Office, Vietnam officially entered the aging stage in 2011 and is expected to become an aged society by 2036. Notably, the transition period from an “aging society” to an “aged society” in Vietnam is estimated at only 20–25 years, much faster than Japan (37 years) or many European countries (85–115 years). This creates significant pressure on the social security system and long-term care infrastructure.

At the same time, the shift from multi-generational families to nuclear families is reducing the traditional caregiving role within households. Elderly people are increasingly living independently, especially in large cities. This trend is creating demand for specialized housing models, including senior housing, retirement homes, and long-term care facilities

However, despite the growing demand, the market has not developed accordingly. The reasons are not only related to income levels, but also to legal structures and the way the market is currently defined.

2. Elderly income and affordability gap

2.1. Income structure of the elderly

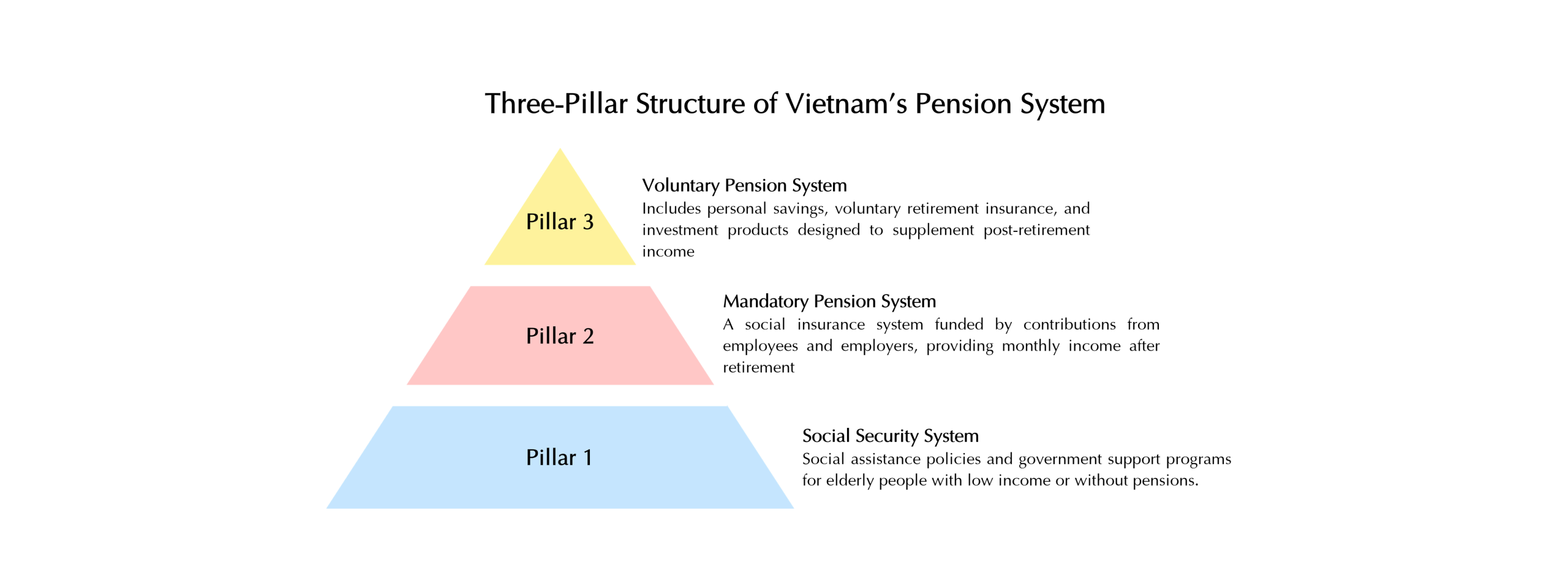

Vietnam’s pension system can be analyzed under a three-pillar structure based on international practice. However, the development level and effectiveness of each pillar differ significantly, directly affecting the affordability of senior housing products.

The first pillar is the social assistance system, which is non-contributory and includes social welfare allowances and social pension support under Decree 20/2021/ND-CP, Decree 76/2024/ND-CP, and Decree 176/2025/ND-CP. Beneficiaries are mainly low-income elderly people without pensions, financial support, or caregivers. The current standard allowance is around VND 500,000 per month, equal to only about 22.7% of the rural poverty line and 17.8% of the urban poverty line. It is also the lowest level within the social security system. According to the Ministry of Health, around 1.5 million elderly people, equal to about 10% of the elderly population, receive monthly social pension support. This shows that the social assistance pillar mainly helps reduce poverty, but it is not sufficient to support participation in specialized housing or care services.

The second pillar is the mandatory pension system, which serves as the main income source for elderly people who contributed to social insurance during their working years. This system follows a defined benefit (DB) model, where monthly pensions are calculated based on contribution years and salary levels. It also operates under a pay-as-you-go (PAYG) mechanism, meaning the working generation finances the retired generation. Currently, around 2.7 million elderly people in Vietnam receive pensions and monthly social insurance benefits, with an average pension of approximately VND 6.2 million per month as of December 2024. Compared with GDP per capita, this pension level equals about 63.2%, which is relatively high compared with many countries in the region, where the ratio is often only 3%–13%. However, this comparison is only for reference because pension systems vary between countries, including Defined Benefit, Defined Contribution, Social Pension, Hybrid, or Notional Defined Contribution models. More importantly, since Vietnam’s pension calculation depends on insured salary levels during certain periods, the actual pension amount remains relatively low, especially when compared with rising living costs and elderly care expenses.

The third pillar is the voluntary pension system, including voluntary retirement insurance, personal savings, and investment assets. This pillar acts as a supplement to the first two pillars. However, it remains underdeveloped in Vietnam because it depends heavily on income levels and financial awareness, while many workers still lack long-term savings capacity or retirement planning habits. Combining all three pillars, post-retirement income in Vietnam remains relatively low, especially for people without stable pensions. As a result, the affordability of senior housing products is limited, reducing market size and affecting the feasibility of investment models in the current stage.

2.2. Cost of elderly care and housing services

Although Vietnam’s pension system may appear relatively strong compared with some ASEAN countries, the reality becomes very different when considering actual living costs, especially elderly housing and care expenses. One of the biggest barriers to the development of senior housing real estate in Vietnam today is the large gap between retirement income and actual service cost. Currently, elderly care facilities in Vietnam charge around VND 8–12 million per month for basic services, VND 15–25 million for mid-range services, and up to VND 30–40 million for high-end services. Compared with the average monthly pension of around VND 6.2 million, these costs are clearly beyond the affordability of most elderly people.

The cost issue is not limited to nursing homes. It also affects senior housing models, especially specialized apartments or retirement communities. Although this segment has not yet clearly developed in Vietnam, references from serviced apartments or pilot projects show that rental prices and ownership costs are still relatively high, often not much lower than mid-range nursing homes. This means that even housing products without medical care, but with elderly-friendly facilities and support services, remain beyond the affordability of most people, especially those without significant financial savings.

As a result, Vietnam’s senior housing market currently serves only a small group of high-income residents, while most potential demand remains unmet. This clearly reflects the “middle gap” problem, where elderly people have real housing needs but are trapped between an underdeveloped pension system and service costs that are positioned at a higher segment to ensure operational efficiency. Compared with countries such as Thailand, where service costs are more aligned with average income levels, Vietnam faces rising costs due to the small market scale and lack of standardization. This makes mid-range models difficult to develop and limits the expansion of the market. Similar affordability and accessibility issues can also be seen in early-stage markets such as China.

| Nursing home | Location | Cost (VND million/month) |

Beds per room |

|---|---|---|---|

| Phương Đông Asahi | Hanoi | 39 | 4 |

| Lotus | Hanoi | 13-30 | 1-4 |

| ALH | Hanoi | 13-24 | 1-10 |

| Tuyết Thái | Hanoi | 8-30 | 1-3 |

| Bình Mỹ | HCMC | 15-23 | 4-5 |

| Javilink | Hanoi | 10-18 | 1-12 |

| Nhân Ái | Hanoi | 9-18 | 1-8 |

| Bách Niên Thiên Đức | Hanoi, Vung Tau, Đong Nai | 7-18 | 1-9 |

| Vườn Lài | HCMC | 10-16 | 2-6 |

| Tâm An | HCMC | 11-15.5 | - |

| Diên Hồng | Hanoi, Phu Tho, Hung Yen, Hai Phong | 7-15 | 1-8 |

| Orihome | Hanoi | 8.5-15 | 1-7 |

| Thanh Xuân | Hanoi | 8-15 | 1-8 |

| Damoca | HCMC | 6-8 | 4-6 |

3. Limited supply and lack of a market-oriented structure

Vietnam currently has more than 370 elderly care facilities, including around 120 public facilities and over 250 private facilities. However, they only meet approximately 1–2% of actual nationwide demand. The network is unevenly distributed, mainly concentrated in Hanoi and Ho Chi Minh City, while many mountainous, rural, and provincial areas still have almost no formal elderly care models. Although the system is expanding with participation from public organizations, private investors, religious groups, and local communities, it still lacks consistency in scale, quality, and operating standards. Some facilities are professionally developed, but most remain small in scale and do not have specialized design standards for elderly residents. As a result, service quality and care experience vary significantly.

More importantly, the market still lacks a clear classification system based on care levels, unlike developed countries where models such as independent living, assisted living, and nursing homes are clearly defined. In Vietnam, most facilities are still generally referred to as “nursing homes” regardless of service level. This prevents the market from forming a clear product structure. As a result, there are no standardized products, no clear pricing benchmarks, and no reliable financial indicators such as yield rates. This not only reflects the early-stage nature of the market, but also shows that senior real estate in Vietnam is still mainly viewed as a social welfare service rather than an investment asset that can develop under market mechanisms.

4. Legal gaps: The core issue of the market

4.1. Current legal framework in Vietnam

In Vietnam, the legal framework related to elderly people is relatively complete from a social welfare perspective. The main legal foundation is the Law on the Elderly (2009), which remains in effect and has not yet been replaced. Other related regulations are included in laws such as the Social Insurance Law 2024, Population Law 2025, and social assistance decrees including Decree 20/2021/ND-CP, Decree 76/2024/ND-CP, and Decree 176/2025/ND-CP, together with Decision 383/QD-TTg in 2025 approving the National Strategy on the Elderly until 2035. These regulations generally cover the rights and obligations of elderly people as well as the government’s long-term policy direction.

However, the current legal system is mainly designed under the logic of social welfare and support for vulnerable groups. In contrast, the development of elderly housing and care models under a market-oriented and diversified approach has received limited attention. In practice, nursing homes in Vietnam are mainly regulated under Decree 103/2017/ND-CP on social assistance facilities. This means they are legally viewed as welfare services rather than real estate products operating under market mechanisms.

From a real estate perspective, Vietnam still has no specific legal document defining or regulating “senior real estate.” Related regulations are scattered across laws such as the Land Law, Housing Law, Real Estate Business Law, Investment Law, and Enterprise Law. For example, under the Land Law, elderly care facilities are classified as social infrastructure land and may receive certain land rental incentives from the government. However, these regulations remain general encouragement policies and do not create a strong or clear development mechanism to attract investment. In reality, nursing homes are not considered a priority investment sector. As a result, investors face many barriers, including land access difficulties, limited tax incentives, complicated administrative procedures, and lack of financial support mechanisms.

Existing facilities operate under different models but lack standardized requirements for design, staffing, care procedures, and protection of elderly rights. This leads to inconsistent service quality and potential risks related to safety and dignity.

In addition, current land planning systems do not clearly allocate land specifically for elderly care facilities. As a result, these projects are almost “invisible” within urban and rural development planning. Many local governments still lack clear criteria for approving or attracting investment into this sector. At the same time, Vietnam has not yet developed a specialized system of technical standards, operating standards, and professional ethics for elderly care services. All of these factors show a clear reality: although many related regulations already exist, Vietnam still has not established a complete legal framework for developing senior housing real estate as an independent property segment.

4.2. Comparison with Japan and the United States

Compared with countries that experienced population aging earlier, such as Japan and the United States, the difference is not only the maturity of the legal system, but also how these countries position senior real estate as part of the market structure rather than only as a social welfare service. In Japan, the legal framework related to the elderly has been developed in an integrated and long-term strategic manner, beginning with the Basic Act on Measures for the Aging Society in 1995. This law not only established general directions for employment, income, healthcare, welfare, and living environments, but also created a governance mechanism through the Council on Aging Society Policies. This shows that elderly issues are treated as a national and cross-sector strategy rather than separate policy areas..

Based on this foundation, Japan further developed its system through the Long-Term Care Insurance Act in 1997, creating a sustainable financial mechanism for elderly care services. The system clearly defines insurance beneficiaries, dependency assessment procedures, and service categories. Users only co-pay part of the service cost, usually around 10–30%, while the remaining cost is covered by the insurance fund. This mechanism allows elderly people to access care services at reasonable costs and creates stable demand for the market.

Most importantly, Japan established a specialized legal framework directly related to real estate through the Act on Stable Supply of Residences for the Elderly in 2001. This law clearly defines “service-integrated elderly housing” as a separate real estate product combining housing functions with essential support services. Projects under this category must register with local authorities, comply with barrier-free design standards, and provide mandatory services such as safety confirmation and daily living support. In addition, regulations related to lifetime lease contracts and financial transparency help protect residents and increase investor confidence. Thanks to the combination of legal support, financial mechanisms, and standardization, Japan has successfully created a comprehensive senior real estate ecosystem with multiple product types, from serviced housing to specialized care facilities.

Meanwhile, in the United States, laws related to elderly housing are not concentrated in a single regulation but are instead developed through a highly segmented and specialized system. The foundation began with the Older Americans Act in 1965, which established comprehensive support programs for elderly citizens. At the same time, the Fair Housing Act (1968, amended) and the Housing for Older Persons Act (1995) clearly defined elderly housing concepts, including communities exclusively for people aged 62+ or 55+ communities under specific operating conditions.

One key feature of the U.S. market is the clear classification of senior real estate products based on care levels. Each category is regulated through different licensing systems and legal requirements. For example, assisted living facilities must receive licenses from state authorities and comply with detailed requirements regarding staffing, care ratios, safety standards, and resident rights. Meanwhile, nursing homes are strictly supervised by the Centers for Medicare & Medicaid Services (CMS), which applies rigorous federal standards and mandatory certification systems. In contrast, independent living models are treated as pure residential real estate products, operating similarly to serviced apartments. These models do not require medical licenses but must still comply with housing and accessibility regulations.

This clear classification system, combined with multi-layered legal frameworks and financial support mechanisms, has enabled the United States to develop a strong senior real estate market. With more than 30,000 assisted living facilities and a strict monitoring system, the market achieves high liquidity and supports investment vehicles such as Real Estate Investment Trusts (REITs), where financial indicators and yield rates are standardized and transparent.

5. Lessons and implications for Vietnam

From a comparative perspective, Vietnam’s biggest difference is not simply the lack of regulations, but the absence of a clear legal approach connecting housing, care services, and financial markets – the core foundation needed to develop senior real estate as an independent asset class. Compared with Japan and the United States, Vietnam is still mainly focused on developing a social welfare system and has not yet transitioned toward a market-oriented model for elderly housing.

Therefore, the key lesson for Vietnam is not to fully copy developed-country models, but to gradually build a legal framework suitable for domestic conditions. First, Vietnam needs to officially define “senior real estate” as a separate property category within the legal system. Based on that, the country can develop appropriate design and operating standards. At the same time, a product classification system based on care levels is necessary to support diversified market development. In parallel, financial support mechanisms, including long-term care insurance and co-payment systems, will play an important role in improving affordability and accessibility for residents. Only when these elements are developed together can Vietnam’s senior real estate market move from being viewed as a “social welfare service” toward becoming an investable and sustainable real estate segment.

However, considering that most elderly people in Vietnam still have limited income, current opportunities are concentrated mainly within a small high-income group, especially in major cities. Without a clear legal framework, investors tend to enter the market through lower-complexity models, particularly independent senior housing projects, which are closer to traditional residential real estate and subject to fewer medical licensing requirements. In the long term, as income levels improve and support policies – especially financial and care insurance systems – become more complete, the market may gradually expand toward more complex models combining housing and care services. This transition will likely occur step by step, beginning with smaller and simpler products before eventually developing into a complete ecosystem similar to those found in developed countries.

Overall, the current legal gap is both a short-term barrier and a selective long-term opportunity.

- Vietnam General Statistics Office. (2025). Rapid population aging in Vietnam: Current situation and solutions.

- Vietnam Social Security. (2025). Gradually improving the living standards of the elderly.

- HCMC Social Security. (2025). Approximately 1.6 million elderly people may receive social pension benefits.

- Central Policy and Strategy Commission Information Portal. (2025). Average pension reaches VND 6.2 million per month.

- OECD. (2024). Pensions at a Glance Asia/Pacific 2024. Organisation for Economic Co-operation and Development.

Author & Contact Information:

Ms. Linh Nguyen

Deputy Managing Director

MOF Certified Valuer

📩 linh.nguyen@dcfvietnam.com

📞+84 763 30 44 30

{kind=link}

{kind=link}

{kind=link}

{kind=link}